Summary

The cost of buying a new car in the United States is reaching record levels, with the average price now nearing $50,000. This surge is driven by car companies moving away from small, affordable sedans to focus on larger, high-profit vehicles like SUVs and pickup trucks. As a result, many middle-class and young buyers are being priced out of the market. With high interest rates and rising insurance costs, owning a vehicle is becoming a significant financial burden for many American families.

Main Impact

The most significant impact of this trend is the disappearance of the "budget" car. Only a few years ago, many vehicles were available for under $30,000, but those options are now rare. This shift forces consumers to take on much larger loans that last longer, often up to seven years. While these long-term loans make monthly payments slightly more manageable, they result in buyers paying thousands of dollars more in interest over time. For many, the dream of owning a reliable new car is being replaced by the reality of long-term debt.

Key Details

What Happened

Automakers have intentionally changed their lineups to maximize profits. Larger vehicles like the Ford F-150 or the Chevrolet Tahoe make much more money for companies than small cars like the Ford Fiesta or Chevy Cruze. Consequently, many of the smaller models have been discontinued. At the same time, new cars are packed with expensive technology, such as advanced safety sensors and large touchscreens, which further drives up the sticker price.

Important Numbers and Facts

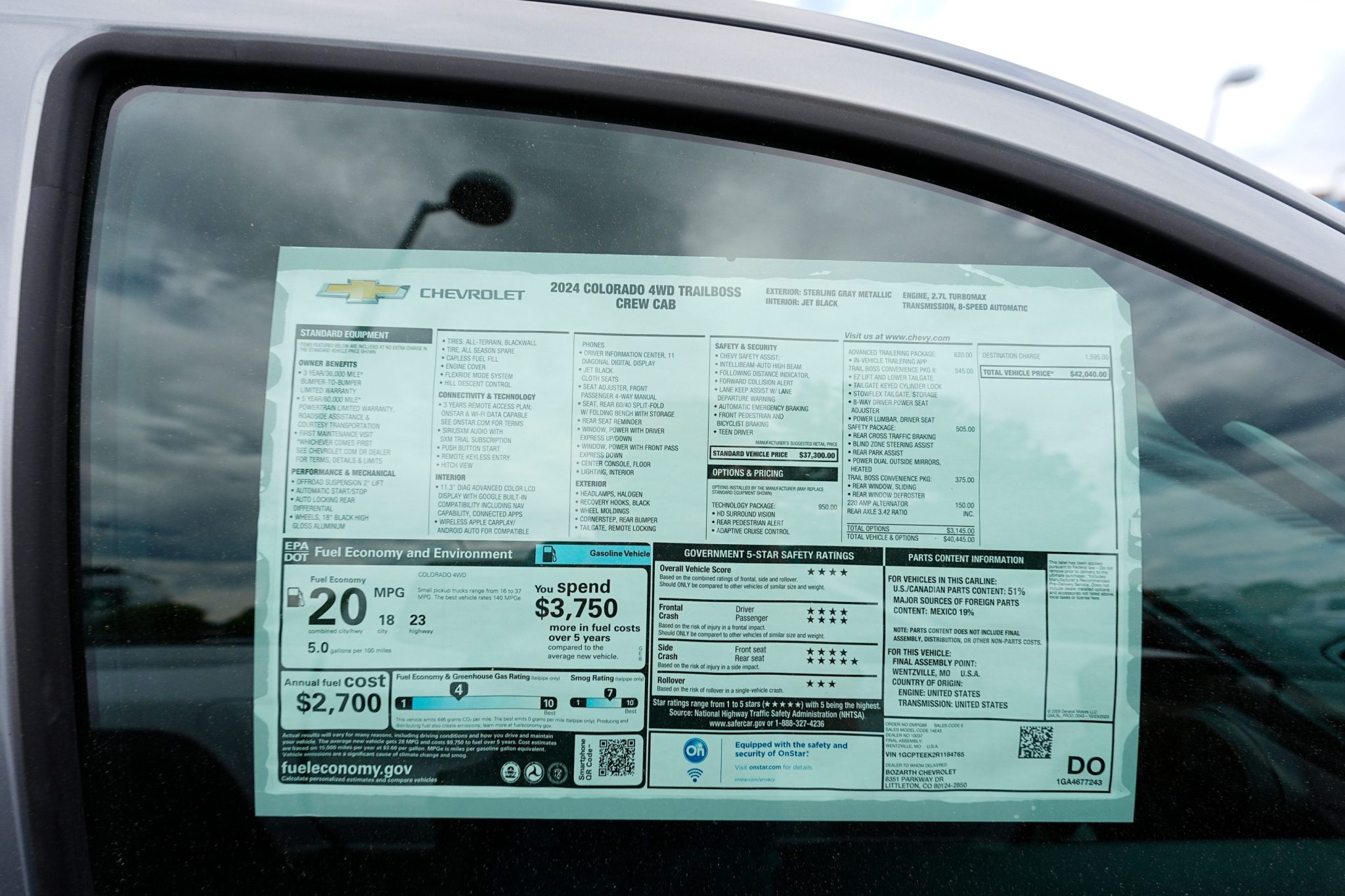

- The average price of a new car has jumped 30% in just six years.

- Average monthly payments for a new vehicle have reached $775.

- Only 13% of new cars are priced under $30,000 today, compared to 40% five years ago.

- New car prices rose by 12.6% over the past year, far outpacing general inflation.

- Car insurance costs have spiked by 55% since 2020, and repair costs are up by 48%.

Background and Context

For decades, car ownership was a basic part of American life, necessary for getting to work and running a household. However, the COVID-19 pandemic disrupted car production, leading to a shortage of vehicles. When production finally returned to normal, car companies realized they could make more money by selling fewer, more expensive cars rather than many cheap ones. Additionally, government regulations now require cars to have more safety features, like backup cameras and automatic braking, which adds to the manufacturing cost. These factors, combined with global supply chain issues and new taxes on imported parts, have created a perfect storm for high prices.

Public or Industry Reaction

Consumers are feeling the squeeze and are changing how they shop. Many people who used to buy new cars are now looking at the used car market. However, even used cars are becoming expensive, with the average used vehicle selling for around $25,000. Some buyers are choosing to pay for cars in cash using their savings just to avoid high monthly interest payments. On the political side, rising costs for cars and gasoline are becoming a major issue for voters. Many young people feel that their wages are not growing fast enough to keep up with the rising costs of transportation, housing, and food.

What This Means Going Forward

In the coming years, the gap between wealthy buyers and everyone else may widen. Some car companies, like Ford and GM, have promised to introduce more affordable models by the end of the decade, but it remains to be seen if these will truly be "budget" options. Another factor is the rise of electric vehicles (EVs). While new EVs are often expensive, a growing number of used EVs will soon enter the market as older leases end. This could provide a new path for buyers looking for lower long-term fuel and maintenance costs. For now, most experts expect Americans to keep their current cars for longer periods—often 13 years or more—to avoid the high cost of a replacement.

Final Take

The era of the affordable new car is fading away. As automakers prioritize luxury and size, the average buyer must decide between taking on heavy debt or settling for an older, used vehicle. This shift is not just about cars; it reflects a broader change in the economy where basic needs are becoming luxury items. For the average family, the road ahead will require careful budgeting and a rethink of what it means to own a vehicle in America.

Frequently Asked Questions

Why are there so few cars under $30,000?

Car companies make more profit on large SUVs and trucks. Because of this, they have stopped making many of the smaller, cheaper sedans that used to be common.

How much has the average car payment increased?

The average monthly payment for a new car is now about $775. Many people are now signing seven-year loans to try and keep these payments from going even higher.

Is it better to buy a used car right now?

While used cars are cheaper than new ones, their prices have also gone up. The average used car now costs about $25,000, and there are fewer used cars available because people are keeping their old vehicles longer.